The UKs Construction purchasing managers’ index remained at a reading of 54.2, unchanged from last month’s figure. This came out higher than the expected figure of 54.0 expanding at its lowest rate for 3 years. While the pace of growth picked up in commercial property and civil engineering, the PMI's gauge of housing construction activity sank to its lowest level since January 2013.

UK Services PMI came out fractionally worse than expected and is an improvement from last month which was nearly its lowest level in three years. Britain's economy appears to have slowed since the start of this year, as worries about the global economy, government spending cuts and a vote on staying in the European Union have had a significant impact. Britain's economy grew 2.3 percent last year. Government forecasters are expecting growth to slow to 2.0 percent in 2016. These factors have all caused the pound to remain weak across the board.

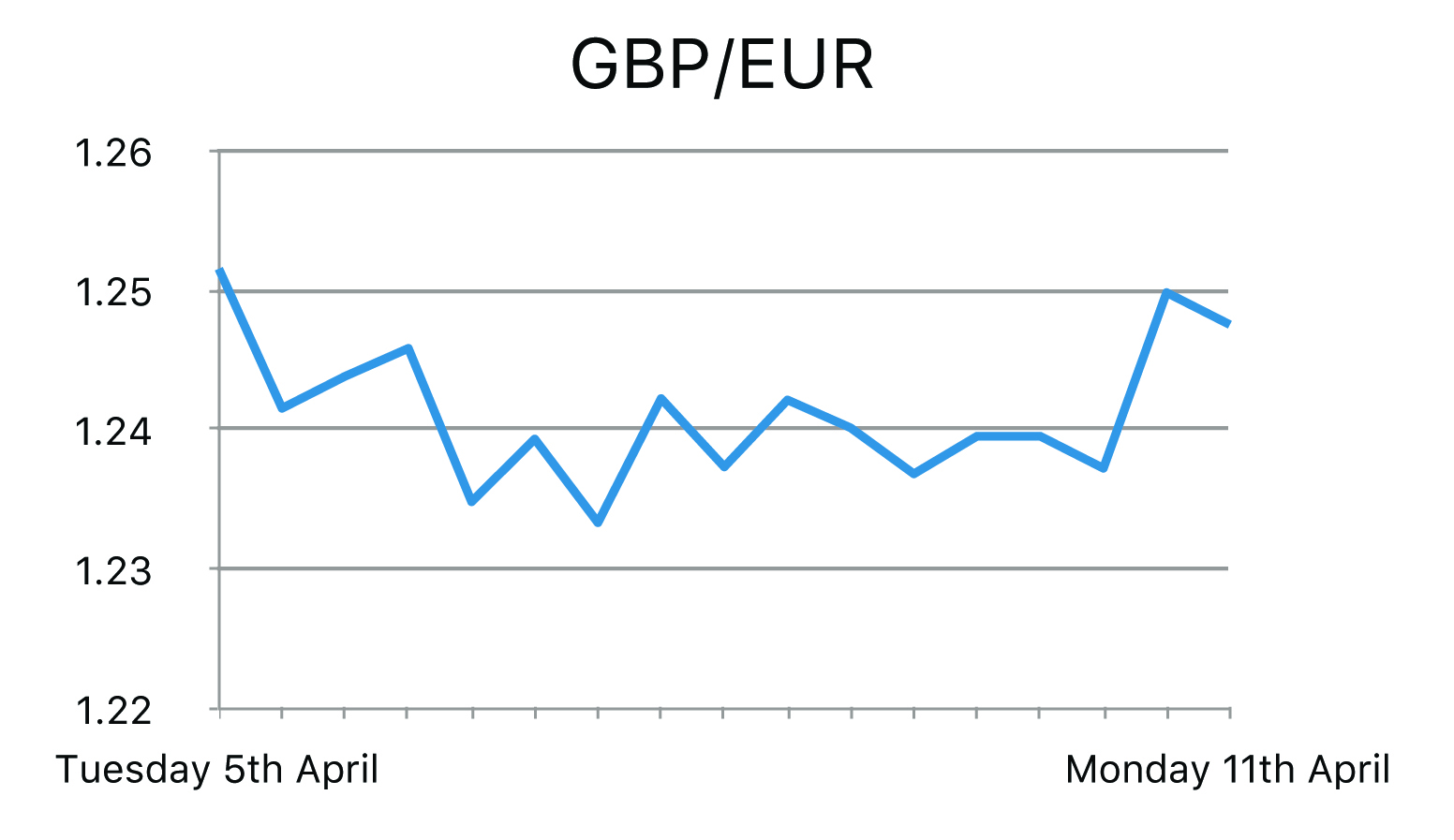

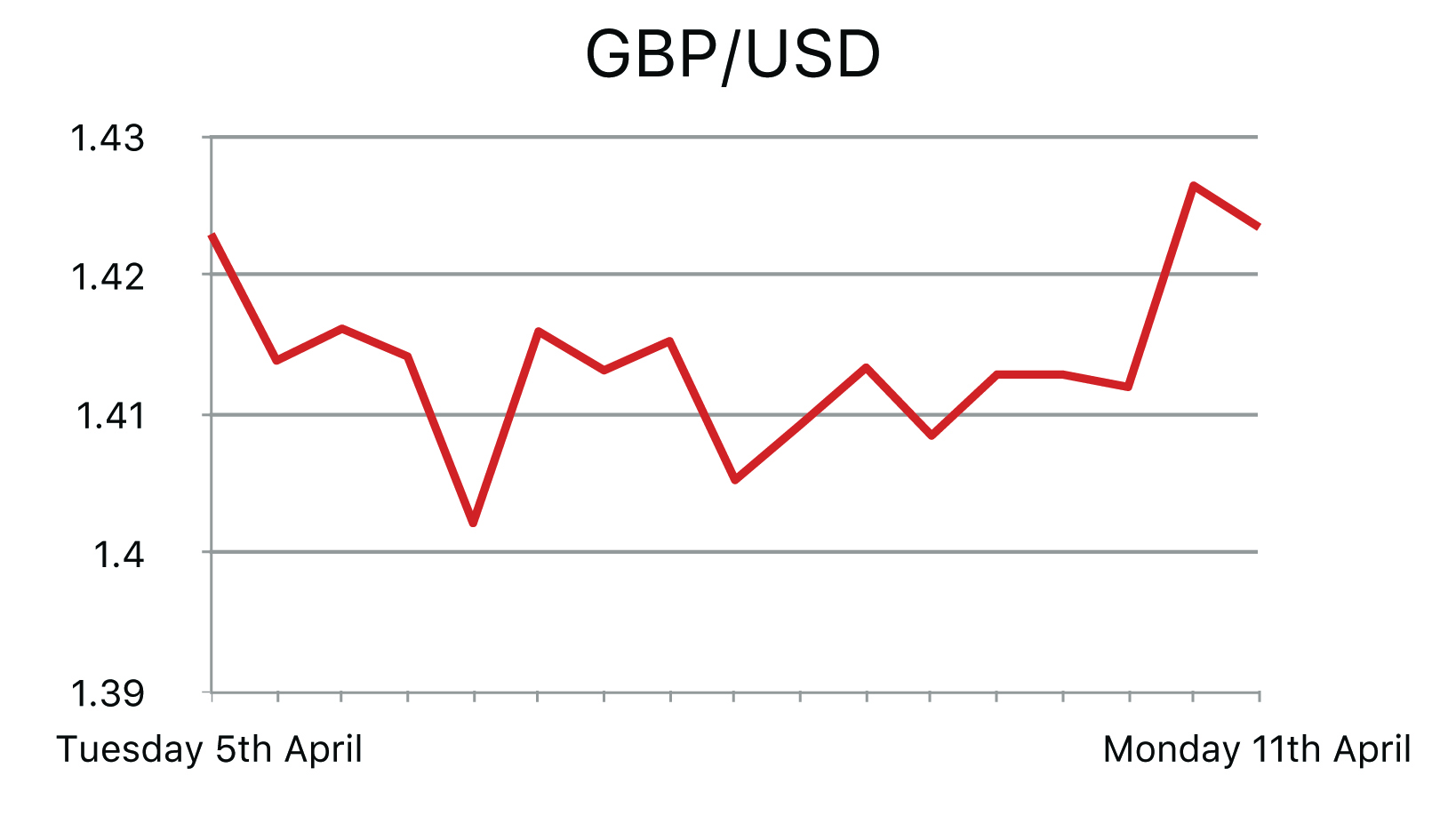

Standard & Poors chief Sovereign ratings officer Moritz Kraemer stated that the Brexit could lead to Britain losing its AAA S&P credit rating which it has maintained since 1978. This would be due to the UKs ‘deep political, financial and trading ties in Europe’ which would be at risk if Britain were to leave the EU. There was an unofficial poll released regarding the Brexit. This Poll indicated a decline in support for the Pro EU parties, indicating quite close race. Thus causing investors to sell the pound as an exit from the Eurozone after the referendum is likely to cause significant economic uncertainty until trade terms with Europe are renegotiated.

However, with investors focused on domestic political and global market risks, fundamental economic data moved in to the background with Sterling climbing from its lowest level in more than two years against a basket of currencies. This move has been widely attributed to improved risk appetite for the pound which gave the Brexit-rattled currency a much needed boost to end four straight weeks of losses. The run up to the referendum on the 23rd of June will prove to be very volatile for GBP especially given that the ‘In’ and ‘Out’ camps are virtually tied before June’s ballot.

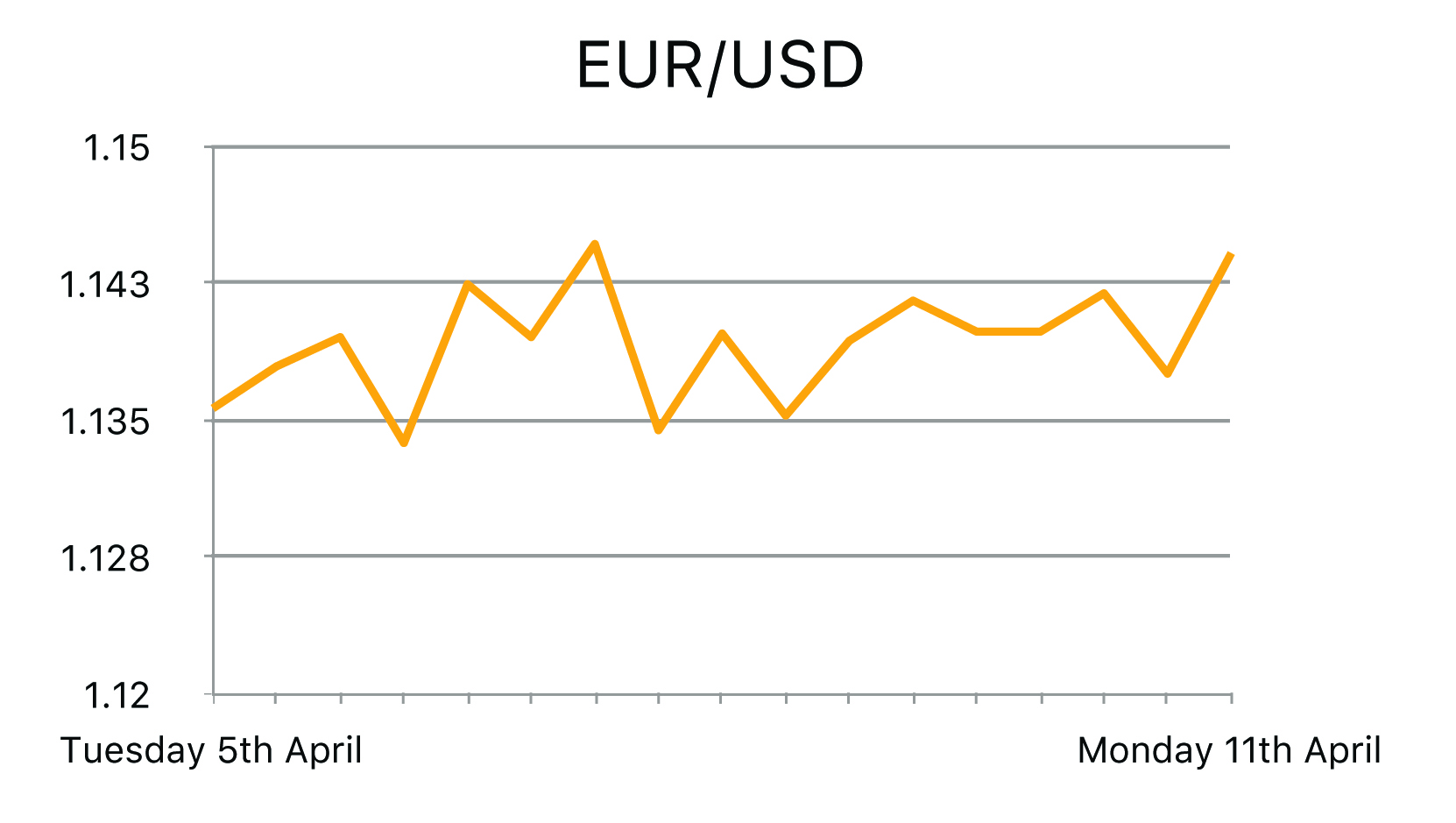

In the Eurozone, unemployment figures were released for February which came out slightly lower than the previous figure of 10.4% coming out at 10.3% which was in line with the expected figure showing a slight contraction in the unemployment rate in the Eurozone. European Central Bank President Mario Draghi said he would keep all options on the table in its fight to stave off deflation in the Eurozone, including sinking interest rates even further into negative territory over the next few months.

The Speech underlines the ECBs willingness to step up its stimulus efforts even though they were increased as recently as its last meeting on March 10. Draghi said that the current stimulus was "without precedent" and was supporting a moderate economic recovery. He said it was time for national governments to start taking steps to make their economies grow faster, producing more demand for goods and services and raising inflation and employment.

In the US, Factory orders came out weaker at -1.7%, well below the previous figure of 1.2% showing contraction of the orders of durable and non-durable goods in the US. This hints at a slowdown in the US economy and may add further weight to the argument that the Fed do not need to raise rates as aggressively this year. We also saw the Labour Market Conditions index released which came out at -2.1, stronger than the previous figure of -2.5 indicating further improvements for the labour market in the US after a solid non-farm payroll figure on Friday. ISM Non-Manufacturing PMI came out better than forecast and was an improvement on last month.

In the weeks passed we have seen the biggest market concerns ease with China’s stock market and yuan crisis, falling oil prices and a strong dollar from US rate hikes all become subdued. Last week Janet Yellen promised caution on any further rate hikes which in turn caused a USD sell off. Emerging markets have steadied with stocks and oil not fall as fast and China’s currency reserves rising again. We may have subsequently seen the recent bout of USD strength and now see the greenback retrace and thus markets become more stable and move back to levels we are more familiar with.