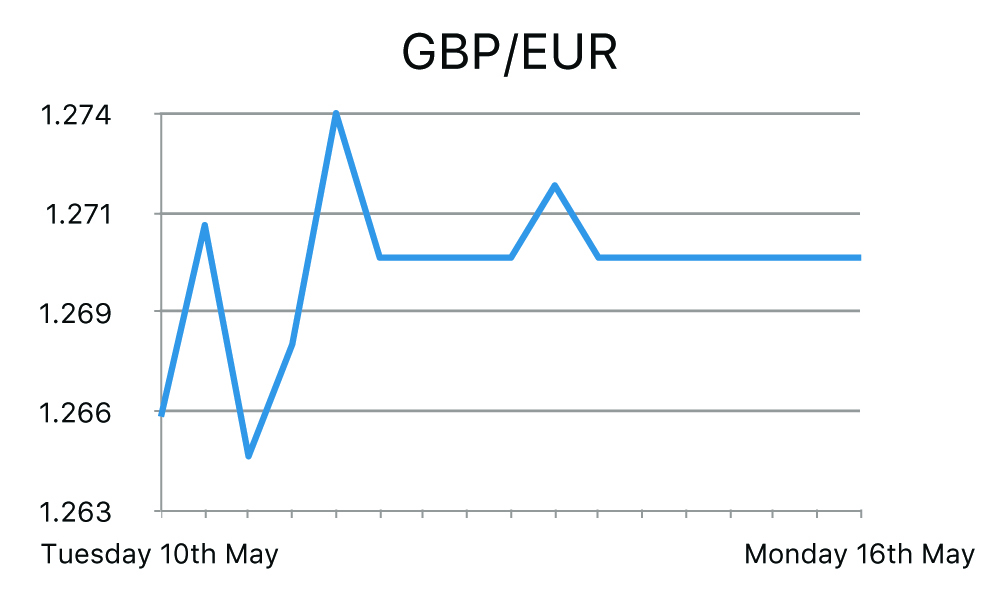

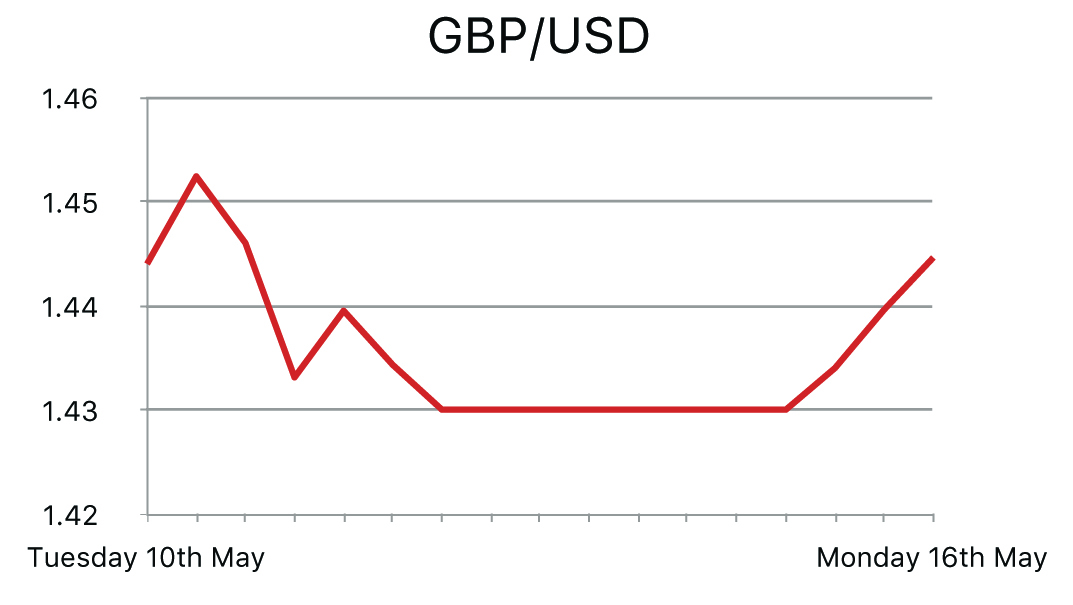

David Cameron and Boris Johnson undertook a sequence of speeches and Q and A’s with regards to the Brexit causing some volatility. During the speech Boris Johnson launched personal attacks on the Prime Ministers ability to re-negotiate terms in the EU accusing him of getting ‘nothing’ from his EU renegotiation and stating he cannot understand why Cameron isn’t campaigning to leave. In addition, Britain's trade deficit has widened in the first quarter of this year by the greatest amount since 2008, signaling the slowdown in world demand is weighing on the UK’s economy.

British economic growth slowed to a quarterly rate of 0.4 percent in the first three months of the year, down from a previous figure of 0.6 in the quarter before - however lower oil prices tend to reduce Britain's trade deficit as the UK is a net importer. Manufacturing production, industrial production and GDP estimates all missed forecasts, although improved on previous readings. Following the industrial production numbers the figures highlighted that the UK industry has fallen back into recession for the third time in eight years, with the main contributors being the fall in steel and iron production.

The office for national statistics stated that production dropped over 37% in this sector compared to a year earlier. Manufacturing also contracted contributing to a slowdown in the overall UK economy, Chris Williamson chief economist at Markit stated, "The goods producing sector therefore looks to be on course to act as a drag on the economy again in the second quarter, contributing to a slowing in economic growth to near stagnation."

Mark Carney issued a hard-hitting analysis of the likely effect of Brexit in the final Super Thursday before the referendum on 23 June and the monetary policy committee (MPC) voted unanimously to maintain interest rates at 0.5 per cent for another month.

The statement triggered an unprecedented attack by former chancellor of the exchequer, Lord Lamont, who questioned Carney's judgement in wading in to the debate, warning he could be responsible for triggering an economic crisis.

The labor market conditions index registered a 0.9 decline for April, after a 2.1 fall the previous month. The fourth successive decline and disappointing trend seen for 2016 as a whole will raise fresh doubts whether the Federal Reserve will be in a position to raise interest rates in the short term. Following the latest declines in March and April, the index has consolidated its position below the zero level, and the index has only dipped twice below this level since the beginning of 2010, potentially indicating a significant peak in the market.

Last week’s headline employment data was weaker than expected, with ADP reporting private-sector job gains of 156,000 for April compared with a consensus of around 200,000; non-farm payrolls increased also below par at 160,000 as unemployment held at 5.0%.

The US jobs figure showed the number of Americans filing for unemployment benefits unexpectedly rose last week to the highest level in more than a year.

Other data also showed import prices increased in April for a second straight month, suggesting that the disinflationary impulse from a strong dollar and lower oil prices, which has helped to hold inflation well below the Federal Reserve's 2 percent target, was fading.

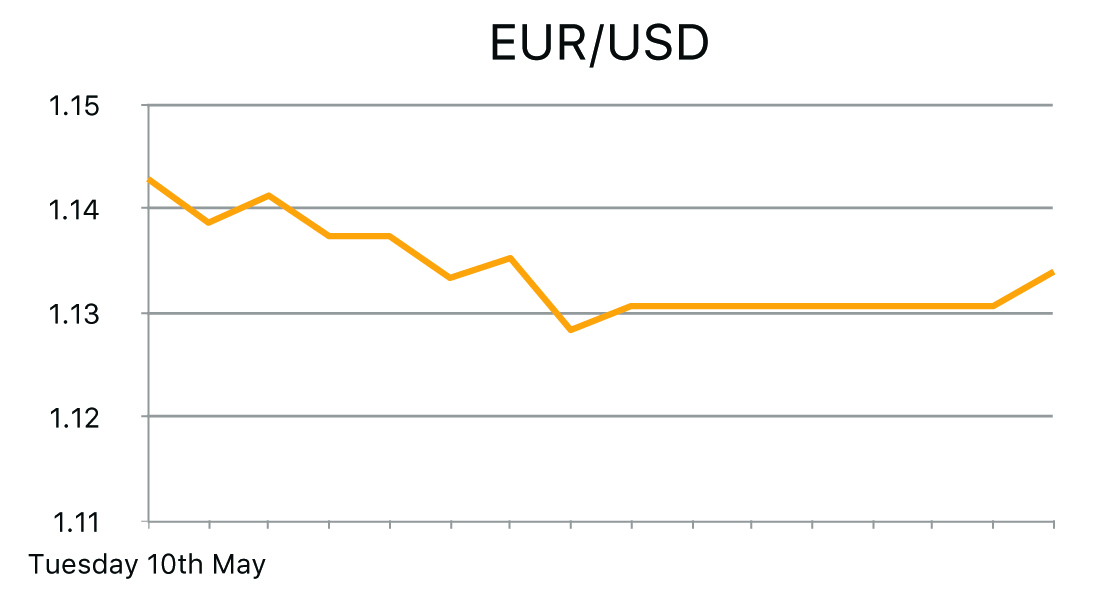

Retail sales jumped in April by the most in a year, indicating consumer spending will help the US economy recover from an early-year slowdown.Healthier household finances, reflecting reduced borrowing and increased savings, mean consumers have the wherewithal to boost spending even as gasoline prices rise and job growth moderates. The Euro group President met the Greek Finance Minister in Brussels yesterday. Greece stated that it is hopeful it will receive the next installment of its bailout loan from Eurozone nations after their talks. However the Euro group still wants Greece to create a privatisation fund and banking legislation before providing the cash. The discussion also concluded that the Euro Zone will offer Greece a form of debt relief from 2017 if it completes reforms by then.

Germany's trade surplus hit an all-time high in March as its exports surged, according data published by the federal statistics office. Exports grew 1.9% while imports fell 2.3%, pushing the surplus to €23.7bn from €20bn in February. Overall, there will be further concerns that Germany is gaining competitive advantage within the Euro area. Further, the substantial trade surplus and weakness in imports will also make it even more difficult to push the Euro weaker against other key global currencies. Lastly, Europe focused on the continuing talks surrounding the Greek debt situation that is taking place in Brussels. Officials are hoping to break a stalemate regarding the €86 billion bailout package with a deadline of May 23rd looming.