All eyes are still on the ‘Brexit’ issue, the week started with Bank of England Governor Mark Carney addressing a cross-party Treasury Committee regarding Britain’s membership of the EU. Carney issued a warning of Brexit risks, highlighting a short-term hit to growth and downturn foreign investment. Mr Carney said: "There could be lower levels of activity because of the degree of uncertainty that could affect investment and household spending.”

Certain members of the Treasury Committee accused him of making ‘pro-EU’ comments however Mr. Carney emphasised that the BoE was not taking sides in the EU referendum. "We will not be making, and nothing we say should be interpreted as making, any recommendation with respect to that decision," he said.

Governor Carney said a vote by Britain to leave the European Union could hit the country's economy and prompt some banks to move away from London's global financial powerhouse. "It's reasonable to expect certain firms would take a view in terms of relocation, and I’d say a number of institutions are contingency planning for that possibility," he said. Economic data was quiet this week but Wednesdays U.K. industrial output data showed that we rebounded in January after a steep drop in December.

Monday saw the factory Orders (YoY) (Jan) released for Germany which came out at 1.1%, increasing from the previous figure of -2.2% and beating the expected 0.0% showing a slight expansion for the German economy in terms of new orders within the economy. Along with that we saw the Producer Price Index (YoY) released for Italy which came out at -2.5% up from -3.2%

In Germany industrial production jumped more than forecast in January as strong domestic demand overpowered the drop in export orders. The output rose 3.3% m/m in January after an upwardly revised 0.3% decline in December. The annualized figure rose 2.2%.

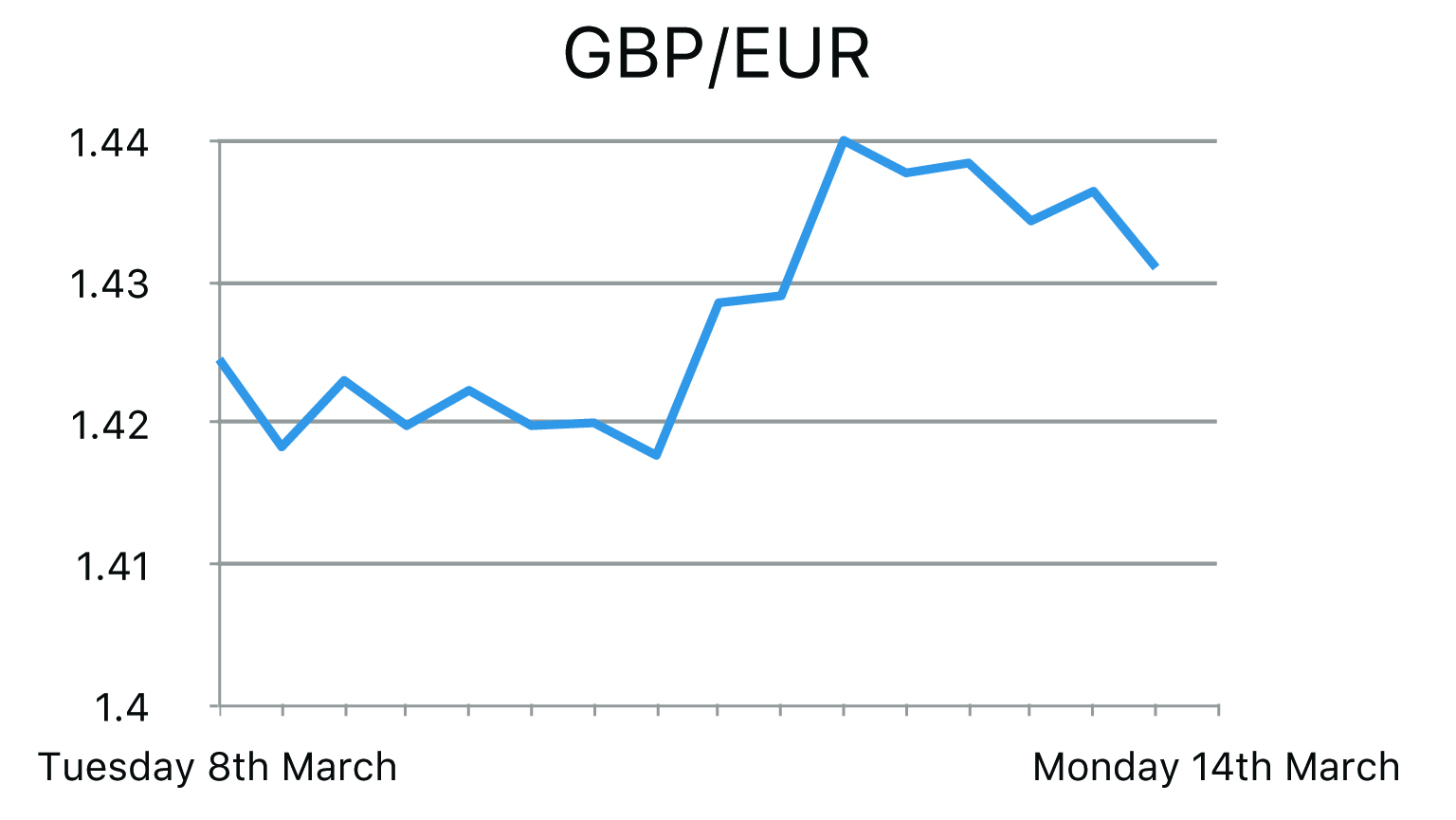

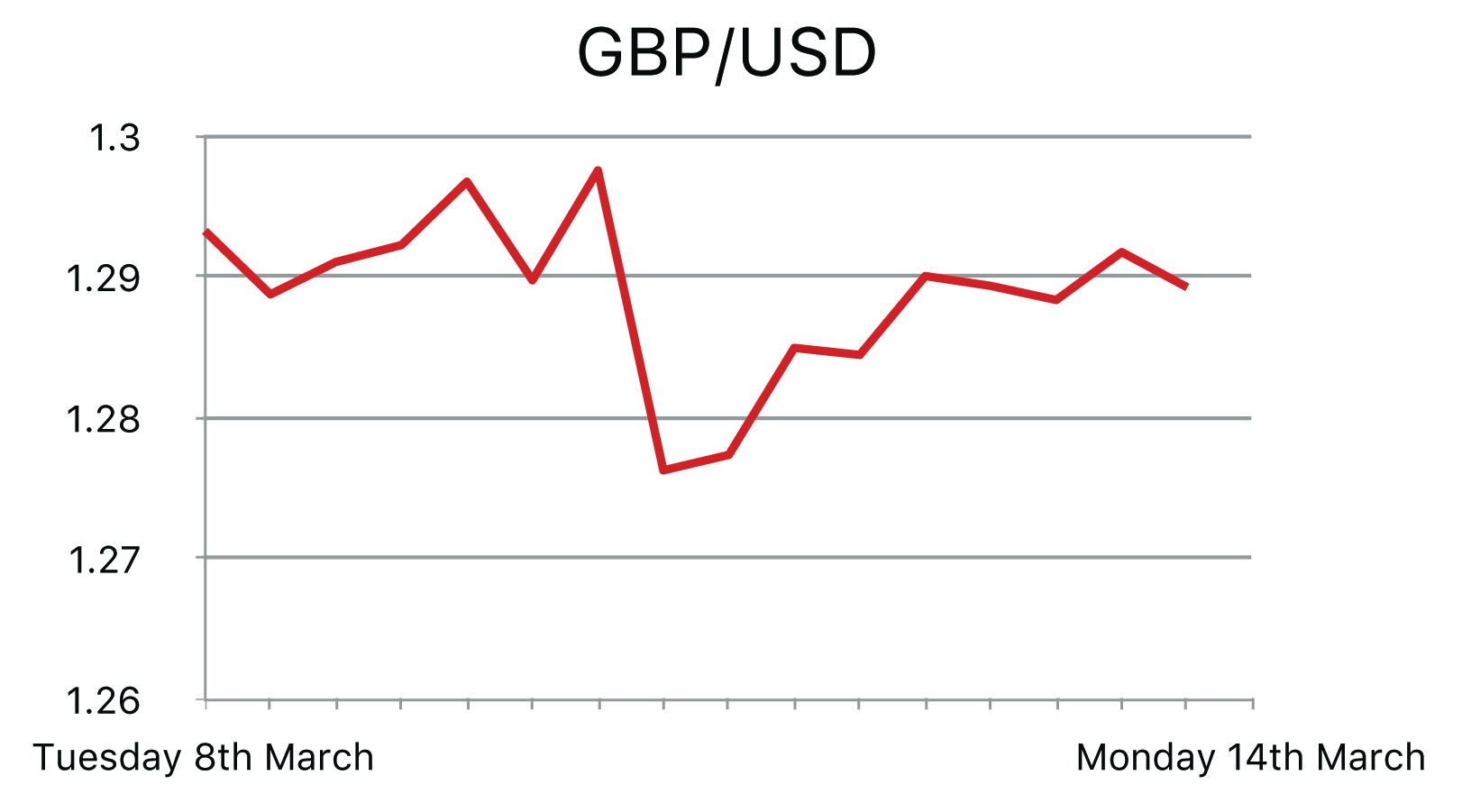

Thursday signalled one of the most volatile days in currency markets following the ECB press conference and rate decision. As expected by markets the ECB cut deposit rates by 10 basis points further in to negative territory to -0.4% which means the ECB will be charging banks more to hold their overnight funds and thus incentivising banks and financial institutions to increase lending activity to ultimately increase economic output. This went hand-in-hand with the marginal lending rate also cut from 0.3% to 0.25% which means banks and financial institutions will be charged less for borrowing from the ECB overnight. Furthermore, Mario Draghi has also increased the quantitative easing programme by €20bn a month, bringing the asset purchase programme to €80bn from a previous of €60bn. This was expected as there was always going to be pressure on the ECB to expand their monetary policy given the single-currency bloc slipped back in to negative inflation for February. Market participants were most surprised by the cut in the ECB base rate to an all-time low of 0.0% from 0.05% amid growing concerns of a fresh economic crash - naturally off the back of this EUR depreciated across the board massively with both GBPEUR and EURUSD reflecting the negative sentiment in the Eurozone given the interest rate cut.

However, the gains made against the EUR were only momentary as in the following press conference Mario Draghi implied interest rates would stay ‘very low’ for at least another year and played down the speculation of further interest rate cuts. As a direct result to these comments; we saw EUR strength return causing EURUSD, GBPEUR and GBPUSD all dramatically retraced the previous gains made. Market participants interpreted Draghi’s comments as positive for the Eurozone as it was insinuated no further interest rate cut was required to boost economic output.

In US the labour market conditions Index kicked off the week with a reading of -2.4 against the previous 0.4. This figure is the lowest recorded since the source was first released in 2014.

Unemployment claims for the US were printed better than forecast as the publication came out showing individuals who filed for unemployment decreased to 259K from a previous 277K, however this data was overshadowed by the ECB meeting. Given the dual mandate operated by the Federal reserve of price stability and employment; the recent unemployment data puts the Fed in a good position to for an interest rate hike when the FOMC meet at the end of this month.

US MBA mortgage application volumes grew 0.20% in the last week, according to data from the Mortgage Bankers Association.